Illinois Teacher Pension Calculator: Plan Your Retirement

Planning for retirement can feel overwhelming, but our teacher pension calculator Illinois makes it so much easier, giving you the confidence to map out your future. The Teachers’ Retirement System of Illinois (TRS) provides a solid pension plan for most public school teachers outside Chicago. It’s like a financial safety net, promising steady income for your retirement years. Still, wrapping your head around all the rules can be a bit tricky.

The Teachers’ Retirement System of Illinois (TRS) covers most public-school teachers outside Chicago and pays a predictable pension. It’s a reliable backstop, but the rules can feel dense. This guide breaks them down and gives you an estimate in minutes. Our TRS pension calculator simplifies it all, helping you estimate your future payout. Ready to get started? Let’s dive in!

Estimate Your Pension Now!Teacher Pension Calculator Illinois

Enter your details to estimate your TRS pension benefits instantly.

Estimated Pension

Monthly Pension: N/A

Annual Pension: N/A

Vesting Status: N/A

FAS capped at $123,489.28 for Tier 2.

This calculator is a simplified estimator and not financial advice. Consult a professional for personalized guidance.

Table of Contents

Key Takeaways

- Pension Formula: Your Illinois teacher pension depends on years of service, final average salary (FAS), and Tier level (Tier 1 or Tier 2).

- Tier Differences: Tier 1 (hired before Jan 1, 2011) and Tier 2 (hired on or after) vary in eligibility, COLA, and FAS calculations.

- Calculator Estimates: Our TRS pension calculator offers quick estimates of your monthly and annual pension, aiding retirement planning.

- Vesting Requirements: Tier 1 requires 5 years of service, while Tier 2 needs 10 years for a lifetime pension benefit.

- Official Source: For precise figures, consult your TRS Member Statement or visit the TRS website.

Why Your Illinois Teacher Pension Matters

As an Illinois teacher, your pension isn’t just a number—it’s your ticket to a stable future. Unlike a 401(k) that swings with the stock market, the TRS pension delivers predictable cash flow. That makes budgeting for your post-teaching adventures way simpler. But let’s be real—questions like “When can I retire?” or “How much will I actually get?” can keep you up at night. Your teacher pensions are a valuable asset, complementing other retirement savings strategies. So, getting a handle on it is a no-brainer.

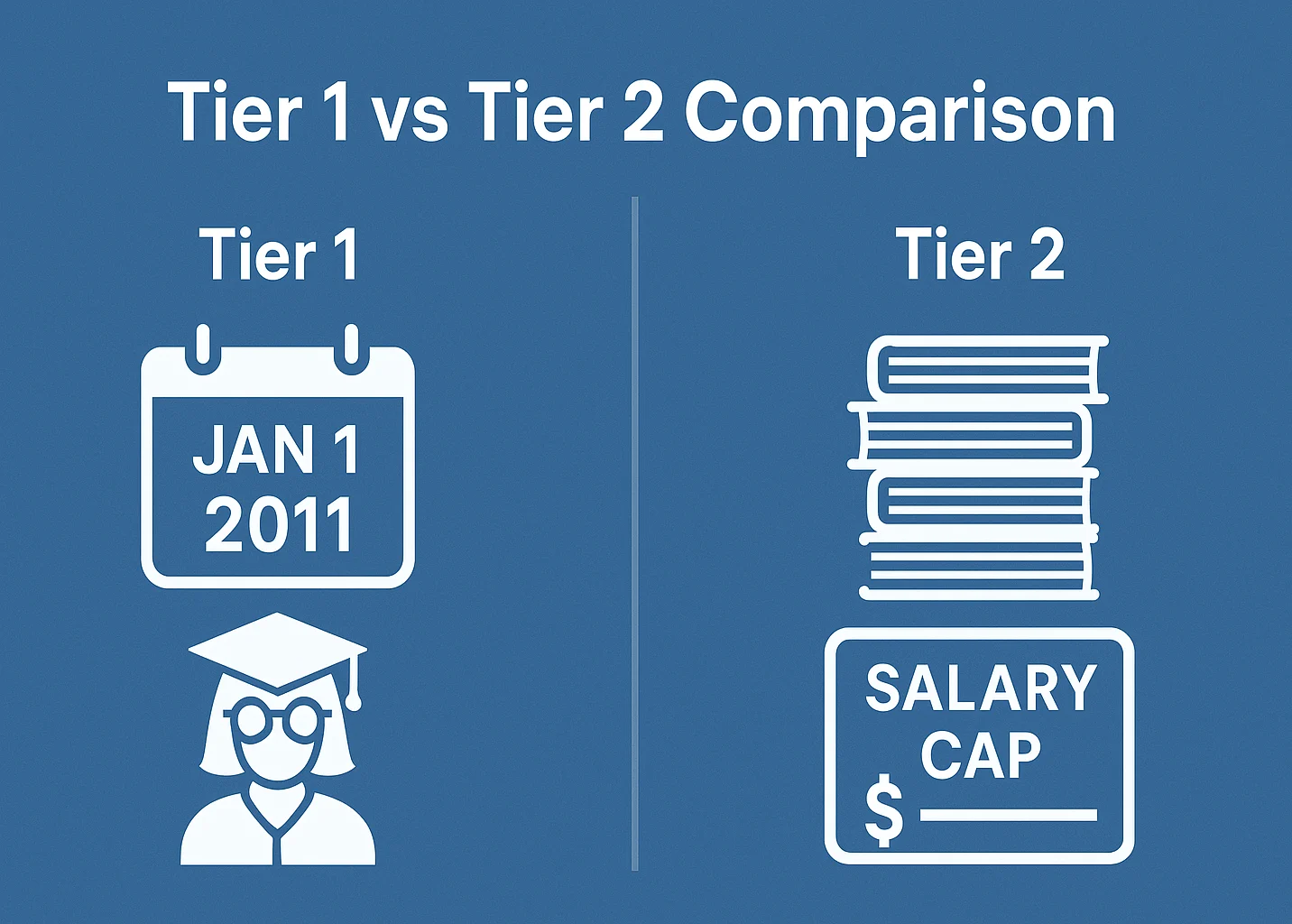

Decoding Illinois Teacher Pensions: Tier 1 vs. Tier 2

The TRS looks after pensions for most Illinois public school teachers, and your benefits hinge on when you started with them. If you joined before January 1, 2011, you’re in Tier 1; if it was on or after, you’re in Tier 2. These tiers change things like when you can retire, how your pension is calculated, and how it grows over time. Let’s break it down nice and easy.

Tier 1: The Classic Pension Plan

If you started with TRS before January 1, 2011, you’re in Tier 1, which comes with some really great perks.

- Full Retirement Age: Age 60 with 20+ years of service or age 55 with 35+ years.

- Final Average Salary (FAS): Average of your four highest consecutive salaries within the last 10 years.

- Benefit Formula: (Years of Service) x (2.2%) x (FAS).

- COLA: 3% compounded annually, starting at age 60 or the fourth January after retirement.

- Vesting: 5 years of service for a lifetime pension.

- Early Retirement: Possible at age 55 with 20–34 years, but a 6% reduction per year under age 60 applies unless you have 35+ years.

Tier 2: Updated Pension Rules

Tier 2, for those hired on or after January 1, 2011, has stricter rules to keep the pension system sustainable.

- Full Retirement Age: Age 67 with 10+ years or age 62 with 35+ years.

- Final Average Salary (FAS): Average of your eight highest consecutive salaries within the last 10 years, capped annually (e.g., $123,489.28 for FY2024; check TRS for FY2025 updates).

- Benefit Formula: (Years of Service) x (2.2%) x (FAS).

- COLA: Lesser of 3% or half the CPI-U, non-compounding, starting at age 67 or the first January after retirement.

- Vesting: 10 years of service for a lifetime pension; otherwise, only a refund of contributions.

- Early Retirement: Possible at age 62 with 10+ years, but a 6% reduction per year under age 67 applies unless 35+ years.

Tier 1 vs. Tier 2 Comparison

Knowing these differences is key to using the calculator. Here’s a clear comparison:

| Feature | Tier 1 (Hired Before 1/1/2011) | Tier 2 (Hired On or After 1/1/2011) |

|---|---|---|

| Full Retirement Age | Age 60 (20 years) or Age 55 (35+ years) | Age 67 (10 years) or Age 62 (35+ years) |

| FAS Calculation | Average of 4 highest consecutive salaries | Average of 8 highest consecutive salaries, with cap |

| COLA | 3% compounded annually | Lesser of 3% or 1/2 CPI-U, non-compounding |

| Vesting | 5 years | 10 years |

| Early Retirement Penalty | 6% per year under age 60 (if <35 years) | 6% per year under age 67 (if <35 years) |

Your Tier is crucial for accurate estimates with this calculator, shaping your retirement age and benefits.

How to Use the Teacher Pension Calculator Illinois

Excited to see what your pension might look like? Our Illinois TRS calculator, one of many handy financial planning tools, gives you a quick estimate based on your info. Take Jane, a Tier 1 teacher with 30 years of service, a $75,000 FAS, and retiring at 60. She used the calculator to project a $49,500 annual pension—then compared a few “what-ifs” to see how an extra year or a raise might shift the number.

Maximizing Your TRS Pension Estimate

To get the most out of the calculator, make sure your inputs are spot-on. Here’s how to do it, alongside solid budgeting habits:

Inputting Years of Service

Add up all the years you expect to work under TRS, including any purchased service credit (like military or out-of-state teaching). Part-time service might count partially, so peek at your TRS Member Statement to be sure.

Estimating Final Average Salary (FAS)

Your FAS is super important but can be a bit of a puzzle. For Tier 1, take your top four consecutive years in the last 10. For Tier 2, it’s eight years, with a salary cap (check TRS for FY2025 updates). Start with your TRS Member Statement and guess your future salary growth.

Choosing Retirement Age

Pick when you plan to retire. Play around with different ages to see how retiring early might shrink your pension. For example, bowing out at 55 instead of 60 as a Tier 1 teacher can take a big bite out of your benefits.

Selecting TRS Tier Level

Select Tier 1 if you were hired before January 1, 2011, or Tier 2 if you started on or after that date. Getting this right is key to nailing your pension estimate.

The calculator’s color-coded status makes results easy to understand:

- Gray: Missing info. 🛑

- Yellow: Early retirement or reduced benefits. ⚠️

- Green: Full pension eligibility—woohoo! ✅

- Red: Not vested yet (5 years for Tier 1, 10 for Tier 2). 🛑

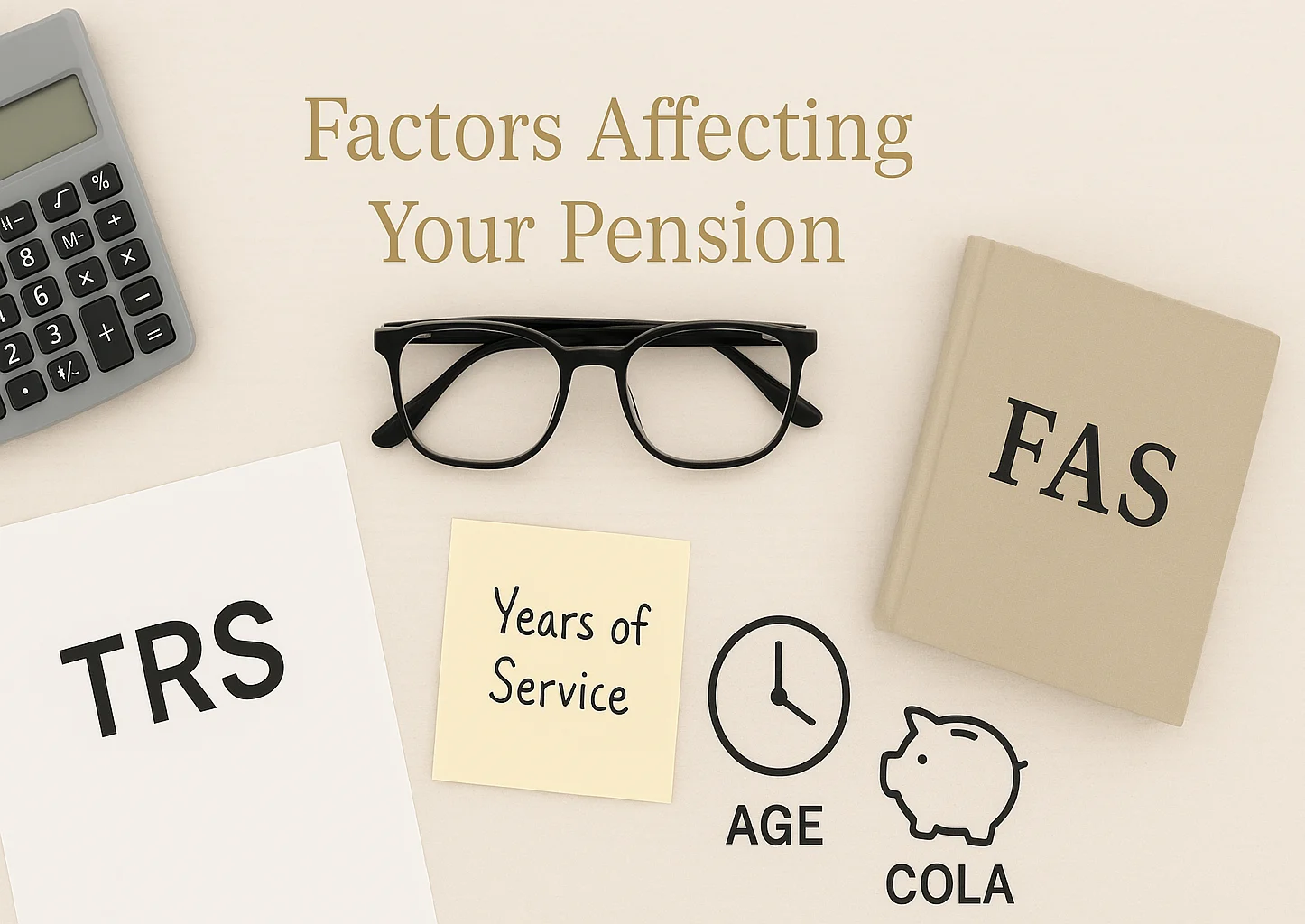

Factors Affecting Your Illinois Teacher Pension

A few things shape your TRS pension, which you’ll see reflected in the calculator.

Years of Service Credit

More years mean a bigger pension, with each year adding 2.2% to your benefit multiplier. Plus, unused sick leave can boost your service credit (up to a limit), and you can buy credit for past teaching or military service.

Final Average Salary (FAS)

A higher FAS pumps up your pension. For Tier 1, focus on your best four years; for Tier 2, it’s the top eight, keeping the cap in mind. Things like earning a degree or taking on extra roles can bump up your salary.

Retirement Age

Hitting the full retirement age (like 60 for Tier 1 with 20 years) maximizes your benefits. Retiring early means a 6% cut per year under that age, unless you meet specific exceptions.

Tier Level

Your Tier sets the rules for eligibility, FAS, and COLA. You can’t switch Tiers, but knowing yours helps you plan smart.

Cost-of-Living Adjustments (COLA)

After you retire, COLA keeps your pension from losing value to inflation. Tier 1 gives you 3% compounded yearly, while Tier 2’s is the lesser of 3% or half the CPI-U, non-compounding, affecting long-term growth.

Strategies to Maximize Your TRS Pension

Want to make the most of your calculator results? Try these tips, paired with good budgeting habits:

- Work Longer: Each extra year boosts your pension, especially if you’re close to full eligibility.

- Increase Salary: Chase raises through degrees or leadership roles, but watch Tier 2’s cap.

- Purchase Service Credit: Buy credit for past service to add years or hit eligibility sooner.

- Use Sick Leave: Turn unused sick leave into service credit, if you qualify.

- Consult Experts: A financial advisor can weave your pension into a bigger savings plan.

Frequently Asked Questions About Teacher Pension Calculator Illinois

Plan Your Retirement with Confidence

Retirement planning is an exciting adventure, and this calculator is your trusty sidekick for early retirement planning. By getting a grip on Tier differences, service years, and salary impacts, you can make smart choices. Teacher pensions are your reward for years of hard work. Start now, estimate your pension, and build a secure, happy future. You’ve earned it! 🍎💰

This content is for informational purposes only and not financial advice. Consult a professional before making financial decisions.